Use our calculator to estimate your monthly mortgage payment, including principal, interest, property taxes, homeowners insurance and even private mortgage insurance — if it’s required. Adjust the home price, loan term, down payment and interest rate to find the right mortgage fit for your budget.

Learn extra payment strategies to pay off your loan faster

A mortgage calculator does all the complex math for you when you’re crunching monthly payment numbers to buy a home. Here’s how each field works:

Home price. If you’ve picked out a house at a specific price, enter that number here. You can also try a range of prices to see how they affect your payment.

Loan term. This is the number of years it’ll take to pay off your loan balance. Choose a 30-year fixed rate for the lowest possible payment, or a 15-year rate if you want to save interest and pay off the balance faster at a higher monthly payment.

Down payment. The more you put down, the lower your mortgage payment will be. If you make a down payment of less than 20%, the calculator will estimate how much private mortgage insurance (PMI) you might pay (this insurance protects the lender in case you default).

Start date. The calculator will default to today’s date if you enter nothing here.

Home insurance. Lenders require you to have enough homeowners insurance to repair or replace your home if there’s a loss from something like a fire or theft. You can also shop for home insurance companies to get the lowest premium.

Mortgage rate. The calculator will reflect the most commonly offered rates. You can check today’s mortgage rates for a more accurate number.

Property taxes. Your property taxes will vary based on your location. You can enter the exact figure if you have it to get a more precise monthly payment estimate.

HOA fees. If you live in a neighborhood governed by a homeowners association (HOA), add the monthly fee here.

Total loan amount. The difference between your home price and down payment.

Total interest paid. The amount of interest you’ll pay over your loan repayment term.

Total of all payments. The total dollar amount you’ll spend for all the expenses included in your monthly payment over the life of your loan.

Total monthly payment. The total amount you’ll pay each month, and the figure the lender will use to qualify you for loan approval.

Principal and interest. How much you’ll pay each month toward your loan balance and interest charges.

Property taxes. The calculator divides your annual property taxes by 12 to calculate this monthly amount.

Homeowners insurance. Your homeowners insurance premium is divided by 12 to calculate this monthly amount.

HOA dues. The HOA fee is included here, if applicable.

PMI. If you make less than a 20% down payment, the estimated monthly PMI charge displays ehre.

There are a lot of decisions to make when you’re buying a home. A mortgage calculator can help you decide whether you should:

The acronym “PITI” is short for principal, interest, taxes and insurance — the four elements that make up your total mortgage payment. Although it’s not required, most homeowners prefer the convenience of having all four components included in their monthly payment.

A few things are worth noting about the PITI calculations included in our mortgage calculator:

Principal and interest calculations are only for 30- and 15-year fixed-rate terms. Ask your lender about 10- or 20-year fixed-term options, or adjustable-rate mortgage (ARM) programs.

Property taxes may change yearly. The tax authorities in your area may adjust your tax rates, which could cause an increase or decrease in your PITI payment.

Homeowners insurance premiums can rise. Be prepared to shop around for homeowners insurance rates every year, especially if you see a jump in your premium.

You may cancel your PMI. Lenders only require PMI if you have less than 20% equity in your home. As your home’s value increases, ask your lender about options to remove your PMI.

HOA fees aren’t paid as part of your PITI. Although you’ll have to pay dues if your home is in an HOA community, lenders only use them to qualify you for your mortgage. You’ll pay the HOA fees directly to the association.

Lenders set limits on how much you can afford to borrow based on your debt-to-income (DTI) ratio — this is a measure of your total debt, including your new house payment, divided by your monthly earnings. Our mortgage calculator is based on conventional loan guidelines, that typically cap your DTI ratio at 45%, although exceptions are possible to 50%.

Here’s a quick example of how to determine whether you can afford a mortgage, assuming your monthly payment is $2,500 and you make $6,000 per month before taxes:

$2,500 monthly payment divided by $6,000 monthly income = 41.67% DTI ratio

Since the conventional DTI ratio maximum is between 45% and 50%, you could afford this payment based on the lender’s guidelines. You can adjust the DTI ratio on a home affordability calculator to get an idea of home prices that fit within your budget.

Try one or all of the following tips to get a smaller monthly mortgage payment:

Choose the longest term possible. A 30-year fixed-rate loan will give you the lowest payment compared to other shorter-term loans.

Make a bigger down payment. Your principal and interest payments will drop with a smaller loan amount and you’ll reduce your PMI expenses. With 20% down, you can eliminate the need for any PMI.

Consider an adjustable-rate mortgage. If you only plan to live in your home for a few years, ask about an adjustable-rate mortgage (ARM). The initial rate is typically lower than fixed rates for a set time period; once the initial low-rate period ends, the rate can adjust based on the ARM term you choose.

Shop for the best rate possible. Studies have shown that comparing quotes from three to five lenders can save you big on your monthly payment and interest charges over your loan term.

Even applying an extra $100 to your mortgage every month can save you thousands in interest charges over the life of a 30-year loan. You’ll also build more home equity with every extra payment.

You’ll instantly see how much total interest you’ll save and how much earlier you’ll be mortgage-free with these three pay-off strategies:

Pay more frequently. With the click of a button, you can see how much interest you’ll save with a biweekly or weekly payment.

Overpay each payment. Use the slider scale to see how much faster you’ll pay off your mortgage by adding up to $500 to your payment every month.

Cash bombs. Use that big work bonus, tax refund or money from another home sale to see how much faster you’ll pay off your loan. You can choose a one-time principal payment, a yearly cash infusion or even choose a quarterly option.

More commonly called a mortgage amortization schedule, the figures below break down the equal installments paid over your loan term. Some important things to understand about mortgage amortization:

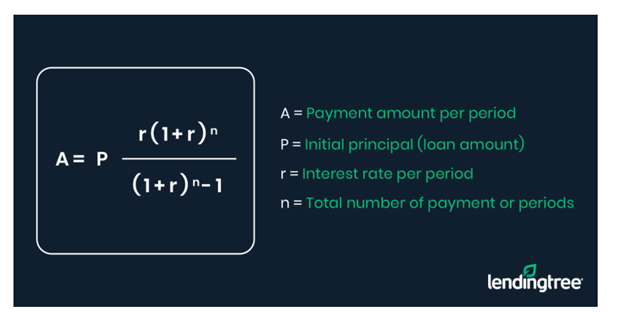

If you’re a math whiz and prefer to make the calculations yourself, here’s the formula embedded in the mortgage calculator: