LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site (such as the order). LendingTree does not include all lenders, savings products, or loan options available in the marketplace.

How to Calculate Your Debt-to-Income Ratio

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It may not have been reviewed, commissioned or otherwise endorsed by any of our network partners.

Your debt-to-income (DTI) ratio — the relationship between your monthly debt payments and gross monthly income — is one of the main factors lenders consider when determining your ability to afford a mortgage.

How to calculate your debt-to-income ratio

There are two types of DTI ratios — the front-end ratio and the back-end ratio. The front-end ratio is the percentage of your gross monthly income used to pay for housing, such as your monthly rent or mortgage payment. The back-end ratio focuses on all your debt, including your housing expenses, and the percentage of your income used to repay it. Mortgage lenders are often more concerned with the back-end ratio, which is what we focus on below.

The following four steps can help you calculate your debt-to-income ratio:

1. Determine your gross monthly income

Your gross monthly income is the amount your employer pays you before taxes and other costs are deducted. Include all documented sources of income when adding up your gross pay amount.

If you’re paid weekly, multiply your weekly gross income by 52, then divide it by 12. If you’re paid every two weeks, multiply your gross pay by 26, then divide it by 12. Write down your gross monthly income amount(s).

2. Establish your estimated monthly mortgage payment

Use the PITI calculation to figure out your estimated monthly mortgage payment. The PITI acronym stands for principal, interest, taxes and insurance.

Pull your estimated monthly mortgage payment from your loan estimate. The amount you see should be based on your:

- Principal and interest payment

- Property taxes

- Homeowners insurance

- Mortgage insurance (if applicable)

3. Add up your other monthly debt payments

Make a list of the required amount due for each of your other monthly debt payments, which can be found on your most recent account statements. Include any fixed or variable accounts that are paid each month, such as:

- Credit cards

- Family support

- Personal loans

- Student loans

- Auto loans

This list doesn’t include your utility bills or any miscellaneous expenses.

4. Run the numbers

Add up your estimated monthly mortgage payment and other monthly debt payments and write down the total. Then, divide that total by your gross monthly income amount. You’ll have a decimal number — multiply that figure by 100 to get your DTI ratio calculation.

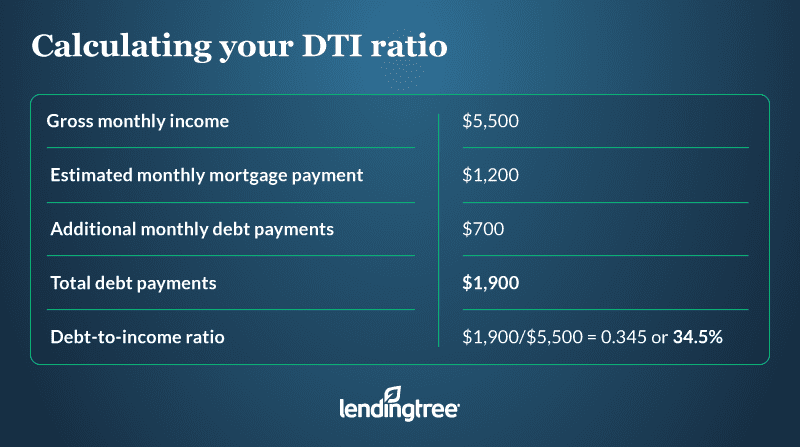

A debt-to-income ratio example

Suppose that your gross monthly income is $5,500. Your estimated mortgage payment is $1,200 and the minimum payments combined on your other debts equal $700, giving you a total monthly debt payment amount of $1,900.

Take the $1,900 amount and divide it by $5,500. The result is 0.345. You would multiply that by 100 to get a DTI ratio of 34.5%. This calculation means you use about 35% of your gross monthly income to repay your total monthly debt.

Why your mortgage DTI ratio matters

Your debt-to-income ratio helps to determine whether you can afford to repay a mortgage. A low DTI ratio demonstrates your ability to manage your existing debt and a new home loan. But a higher DTI ratio can make it harder to qualify for a mortgage because it shows your budget is stretched too thin. In other words, you don’t have enough income to cover more debt.

Mortgage lenders establish maximum DTI ratios as part of their loan approval process. The often-cited rule of thumb is to keep your back-end ratio at or below 43%, according to the Consumer Financial Protection Bureau.

Here are the maximum back-end DTI ratios by loan type:

- Conventional: 45%

- Federal Housing Administration (FHA): 43%

- U.S Department of Agriculture (USDA): 41%

- U.S. Department of Veterans Affairs (VA): 41%

Some lenders may allow a slightly higher DTI ratio — up to 50% in many cases — if you have compensating factors, such as a higher credit score or larger down payment.

Does your DTI ratio affect your credit score?

The short answer is no, your DTI ratio doesn’t impact your credit score. However, there are factors on your credit report that play into your DTI ratio. Your minimum payments, which are reported to the credit bureaus by your creditors and lenders, are used to help calculate your DTI ratio. So the less debt you owe, the lower your DTI ratio is likely to be, which may even lead to a higher score.

What does affect your credit score is the amount of debt you owe — accounting for 30% of your score calculation. Specifically, your credit utilization ratio, which is the percentage of your available credit that’s in use, can impact your score. Similar to your DTI ratio, the lower your credit utilization ratio, the better. It’s wise to use no more than 30% of your available credit on each account and altogether.

4 ways to improve your DTI ratio

- Reduce your credit card balances. If you’re close to the limit on any of your credit cards, pay down those balances. Let’s say your card has a $1,000 credit limit. Your credit utilization shouldn’t exceed $300. Not only does this help improve your credit score, but it can lower your minimum credit card payment and possibly your DTI ratio.

- Pay off any debts you can. If you have a credit card or loan account with a relatively smaller balance, focus on getting rid of that debt before applying for a mortgage — if you’re able to do so. That way, there’s at least one less monthly debt payment to add to your DTI ratio calculation.

- Increase your income. Consider taking on a part-time job or side hustle. This can increase your annual earnings and ultimately lower your DTI ratio.

- Ask questions. Don’t be afraid to reach out for help. If a mortgage lender tells you that your DTI ratio is too high, don’t give up — ask about other mortgage programs you may qualify for and suggestions for reducing your debt load.